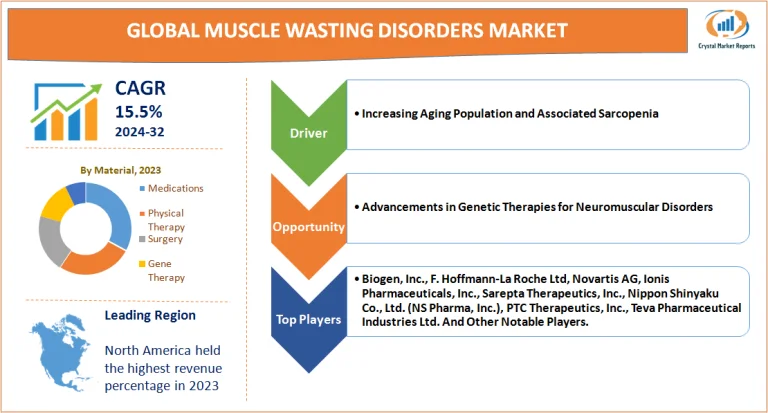

Market Overview

Muscle wasting disorders, characterized by the significant reduction of muscle mass and strength, have been the subject of increased medical attention over recent years. These conditions encompass a variety of diseases ranging from sarcopenia, typically related to aging, to neuromuscular disorders like muscular dystrophy. The muscle wasting disorders market is estimated to grow at a CAGR of 15.5% from 2024 to 2032.

Muscle Wasting Disorders Market Dynamics

Driver: Increasing Aging Population and Associated Sarcopenia

One of the primary drivers for the muscle wasting disorders market is the exponential rise in the global aging population. As the baby boomer generation enters the senior age bracket, the prevalence of sarcopenia — a muscle wasting condition closely associated with aging — has surged. According to the United Nations' report on World Population Aging, the number of individuals aged 60 years or older is expected to double by 2050. This demographic shift has led to an uptick in cases of sarcopenia. Compounded by the fact that muscle wasting exponentially increases the risk of physical disabilities, falls, fractures, and overall mortality, the healthcare industry's focus on combating this disorder has intensified. Treatment strategies ranging from hormone replacement therapies to strength training regimens have garnered attention, signifying the market's expansive potential.

Opportunity: Advancements in Genetic Therapies for Neuromuscular Disorders

The realm of genetic therapies has showcased promising results in addressing the root causes of certain muscle wasting disorders, especially those of a hereditary nature like muscular dystrophy. Recent case studies highlight instances where gene therapies have been successful in introducing or correcting specific genes, leading to improved muscle function and reduced disease progression. For instance, a publication in the New England Journal of Medicine detailed a gene therapy trial that demonstrated improved motor functions in children with a specific type of muscular dystrophy. As genetic research continues to unveil the underlying mutations causing these disorders, the opportunity to develop targeted therapies expands, potentially revolutionizing the treatment landscape.

Restraint: High Treatment Costs and Limited Accessibility

While advancements in treatment and management are promising, they come at a steep price. The costs associated with cutting-edge treatments, especially genetic therapies, are exorbitant. Many of these treatments are not universally covered by insurance, placing a significant financial burden on patients. Furthermore, the limited availability of specialized treatment centers, primarily in low-to-middle-income countries, restricts access to care. A study in the Journal of Clinical Medicine emphasized the significant disparities in the availability of neuromuscular disorder treatments across different regions, elucidating the market's challenges in achieving global reach.

Challenge: Variability in Clinical Presentation and Diagnostic Difficulties

Muscle wasting disorders present with a wide variability in clinical symptoms, often making early diagnosis challenging. Given that timely intervention is crucial to manage progression, this diagnostic delay can lead to compromised patient outcomes. Muscle biopsies, one of the gold standards in diagnosing certain muscle-wasting disorders, are invasive and might not always provide conclusive results. An article in the Muscle & Nerve journal highlighted instances where muscle biopsies yielded non-specific results, necessitating further diagnostic procedures. This variability not only prolongs the diagnostic journey but also amplifies the emotional and financial distress associated with these disorders.

Market Segmentation by Type

In terms of revenue generation, muscular dystrophy led the market segment in 2023. This can be attributed to its prevalence, especially in the pediatric population, and the high costs associated with its management, which include physiotherapy, surgical interventions, and medications. The research focus on dystrophic conditions, especially Duchenne Muscular Dystrophy (DMD), has paved the way for innovations in treatments like gene therapies and exon skipping drugs, further pushing the revenue envelope. In contrast, muscular atrophy, often a consequence of neuromuscular diseases or conditions like ALS, spinal muscular atrophy, or nerve injuries, demonstrated the highest Compound Annual Growth Rate (CAGR). The rising awareness, early diagnostic interventions, and burgeoning therapeutic pipelines for conditions like Spinal Muscular Atrophy (SMA) contribute to this growth trajectory, expected to continue from 2024 to 2032.

Market Segmentation by End-User

In 2023, hospitals emerged as the principal revenue contributor for the muscle wasting disorders market. This dominance was attributed to the comprehensive care offered, including diagnostics, therapeutics, surgeries, and rehabilitation, all under one roof. As multidisciplinary approaches became essential for managing these disorders, hospitals' holistic care model was preferred. However, from 2024 to 2032, it's expected that rehab centers will showcase the highest CAGR. As the emphasis shifts towards improving quality of life, maintaining mobility, and delaying disease progression, the role of rehabilitative therapies in muscle wasting disorders management becomes paramount. These centers, specializing in physiotherapy, occupational therapy, and speech therapy, among others, are becoming increasingly pivotal. Specialty clinics, focusing on niche therapeutic areas, and other segments like home care also play crucial roles, with patients seeking personalized, specialized care or preferring treatments within the comfort of their homes.

Market Segmentation by Region

North America, with its advanced healthcare infrastructure, research initiatives, and patient awareness, held the largest revenue share in 2023. The FDA's approval of drugs for conditions like DMD and SMA, coupled with the presence of major pharmaceutical players, propelled the region's dominance. However, the Asia-Pacific region is anticipated to exhibit the highest CAGR from 2024 to 2032. Factors like increasing healthcare expenditure, rising awareness of muscle wasting disorders, and improving diagnostic infrastructure contribute to this forecasted growth. Moreover, the burgeoning population and the presence of untapped markets present lucrative opportunities for market expansion in this region.

Competitive Trends

The muscle wasting disorders market is characterized by intense competition, with major players like Biogen, Inc., F. Hoffmann-La Roche Ltd, Novartis AG, Ionis Pharmaceuticals, Inc., Sarepta Therapeutics, Inc., Nippon Shinyaku Co., Ltd. (NS Pharma, Inc.), PTC Therapeutics, Inc., and Teva Pharmaceutical Industries Ltd. leading the charge in 2023. These companies primarily focused on strategies like mergers, acquisitions, research collaborations, and aggressive R&D investments to maintain their market positions. For instance, Roche's acquisition of Spark Therapeutics accentuated its foothold in the gene therapy arena, especially concerning muscle wasting disorders. Additionally, the emphasis on patient assistance programs, ensuring drug accessibility even with high costs, became a notable strategy. Moving forward, from 2024 to 2032, it's expected that these players will continue their innovations, collaborations, and strategic alliances, driving the market forward.